Investing Style and Perspectives

For #Fintwit India , the favorite whipping boy for a while has been Momentum. While its usual to get whipped when one is on the losing side, this time around even winning doesn’t seem to matter for the guys who follow this methodology are being whipped for paying taxes on their profits.

Most of the persons on the other side follow Value Investing even though there are as many divisions on what exactly constitutes value. Is buying Reliance Communications when it is below a Rupee constitute buying a crap company or a Cigar butt investing?

Its hurting to see a strategy that one believes in ridiculed and more so by guys who seem to confuse between systematic momentum and random buying but calling it momentum.

But the more I interact with people on the other side of the fence, the more I appreciate what they are trying to achieve. It’s not something I may do though there is always a itch to try and identify a stock well before the market as a whole does.

Size is a limiting factor for Momentum. Most fund managers on the other hand are managing money on a size that is 100 or even 1000 times more than what an optimal AUM for momentum would be. There is just no way that even if they somehow were to become believers in momentum can execute the same without slippage killing them.

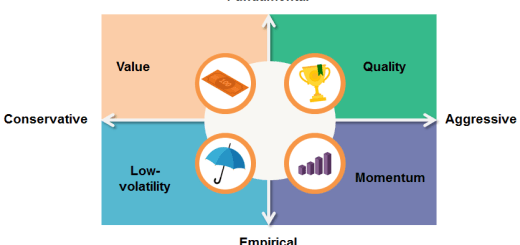

Almost all great investors one can name can be bracketed as Value investors – it could be deep Value or Growth at Reasonable Valuations or any of the other nuances they may wish to identify with but the approach they take is one where the Valuation of the business takes a predominant role.

All intelligent investing is value investing says Charlie but what is “intelligent investing” anyways. Last year, I bought Tata Elxsi as one of my portfolio stocks. I continue to hold the stock which is up 200% from where I bought. If given no context on how I bought the stock, does it merit being an intelligent investment? Afterall, as Charlie says, all good investing is value investing.

The objective of all styles of investing comes down to managing Risk. Value investing does that by way of buying securities where the buyer sees a margin of safety. A momentum investor on the other hand limits his risk by cutting down on stocks that lose out on momentum.

We have been doing things that are contrary; the things that people tell us won’t work from the beginning. In fact, the only way to get ahead is to find errors in conventional wisdom

Larry Ellison

One of the biggest reasons for why a lot of investors fail is peer pressure. Pressure to do things like the winners do even though they lack the resources that are available to the big guys. Coat tailing is rampant but given our lack of understanding on the reasons and more importantly portfolio construction of the investor we wish to coat tail, our returns will almost surely be worse than the person we are attempting to copy.

Peer pressure of doing things similarly is not limited to investing either. The other day, I, with a friend of mine, visited a famous dosa hotel in Bangalore. If one were to try and list the most famous dosa hotels in Bangalore, this would come Second or Third. The first is so famous that the waiting time these days can be as much as an hour.

One of the trademarks of the most famous dosa hotels is the way the dosa is carried by the server as he comes to serve the customers. Multiple dosas are piled up on one another making it in itself something of a curious sight of its own.

The dosa hotel I went to never had this kind of serving. Dosa’s were brought mostly in a tray and served to the customers. But this time I could see a difference. The server brought in about half a dozen or more dosas piling it one top of the other. But he was when he reached the table next to us clearly uncomfortable and afraid of spilling it all. He asked the customers themselves to reach out and take out the dosas slowly and only when it was reduced to a couple was he more comfortable.

My friend commented on this about how despite being well known, even the hotel was getting driven by peer pressure of doing something that they weren’t in reality comfortable just to make it more similar to the more famous hotel.

Thinking about it made me wonder as to how much of this was related to investing. First we have this benchmark that we wish to beat. Then of course, there are always other guys whose returns we wish to beat.

The pressure of a friend being able to generate a higher return most of the time forces the others to take more risks that they are comfortable with in the first place for what if one’s returns are lower – it would make one look bad or worse.

The pressure of wanting to get rich and rich fast is what attracts most people to derivatives, even those who know that in the long run (which may not be that long in the first place), most derivative traders have blown up their capital many times over. Yet, the attraction of what seems like an easy endeavor from the outside makes one keep trying before most quit – some when they aren’t too behind in the game while many when they are thrown out once and for all. No one really quits when it is working for who does that.

Momentum Investing is fascinating for clients for it seems to suggest that there is a possibility of making a great deal of money, more than what you could do otherwise if you just stick with the system. How hard it is to make the changes once a week or a month says the newbie.

But there is no free money, not in Momentum, not in Value or in Quality. Whatever the additional returns that a strategy makes can most of the time be drilled down to higher risks that were taken and one that got paid.

It’s been five years since I started investing by way of systematic momentum, 15 if I count the number of years I have been a follower of systems (trading and not investing in the past). I think I have a better understanding of the strategy today vs 5 years back. But the real deal is only once I complete 20 years for then I shall surely know whether I did the right thing by following a strategy that is anathema to most but one I believed shall work out well.

It’s tough to be contrarian, but if one wishes to have results different from the herd, one needs to embrace it and accept that one’s path may not all the time be accepted by the peers whose respect we wish to have.

Recent Comments