Choices, Noise & Investing

Finance is simple. Try to earn more than what you need to spend, save the difference as best as you can. That is what my Parents and their Parents before did. They earned, they saved a bit and invested into assets they were comfortable with.

I have never been to the United States, but I have read much about the choices available to a customer. A quote that got my attention,

A typical Costco store stocks 4,000 types of items, including, say, just four toothpaste brands, while a Wal-Mart typically stocks more than 100,000 types of items and may carry 60 sizes and brands of toothpaste.

Four vs Sixty. There is not even a sense of comparison on what is easy to pick and select. When it comes to finance, from the US to India, it’s moving closer to what we see with Walmart. In 2020 alone, the US saw 318 new ETFs being launched. In the first 7 months of this year we have seen 221 new ETF’s being introduced.

There is a plethora of Blogs, Podcasts, Youtube Interviews, Clubhouse Discussions, Substack that constantly pump out information – way more information that what we need or desire maybe. Choice is good to an extent after which it starts to actually hurt. More choices basically means more options which generally tends to create more confusion. Oh, I left out Television and Pink Papers.

Opinion Makers are dime a dozen. On Twitter, one interesting observation has been that those who tweet a lot get a lot more followers. This even though they may not even have a track record of their own. On the other hand we have Fund Managers and CEOs who have much lower followership.

Noise makes us question our beliefs. From April of last year, the best way for most investors would be to just be invested. But data – the one from Mutual Funds shows otherwise. From April 2020 to June 2021, investors have actually pulled out money and this after accounting for the huge inflow that SIP’s bring in every month.

Some actions may be due to need but the majority is mostly money that was scared out by the constant humming of those who feel that markets are ripe for a meltdown. After seeing one as recently as March 2020, it’s not surprising that those sitting on the edges would want to get out as soon as they saw some recovery from the bottom.

This is not to say that markets may not fall, that they shall fall is guaranteed. But the constant refrain of crash and the accompanying loss of one’s net worth impacts a great deal on one’s ability to handle the smallest of drawdowns.

On the other hand, because I am bullish, continuously pushing that narrative is wrong too for that sets the wrong expectations. The last year has seen a surge of new investors. In markets, these investors have been rewarded plenty.

Investing Now

Does it make sense to add money at the current juncture was a question I received from a subscriber. My standard reply has always been – it doesn’t matter when you invest, the first year of investment is when the risk is at the highest.

Markets since 1986 (when the Sensex started) have closed in positive one year ahead 70% of the time. This is the drift that has meant that a long term investor has a very low chance of losing.

This is not unique to India either. For the same time period, the FTSE Index and the German Dax had a positive return 68% of the time. S&P 500 has an even better record – positive 80% of the time. Since its own inception though, this falls to 74% of the time.

The only exception of course remains the Nikkei. Since 1950, the one year positive return percentage is around 65% and this falls to 55% if you were to start from 1986.

Longer the time period, greater the probability that you shall be positive. For most prominent indices, being invested for 15 years or more has more or less guaranteed positive returns (exceptions being the Dow due to the Great Depression and of course Nikkei).

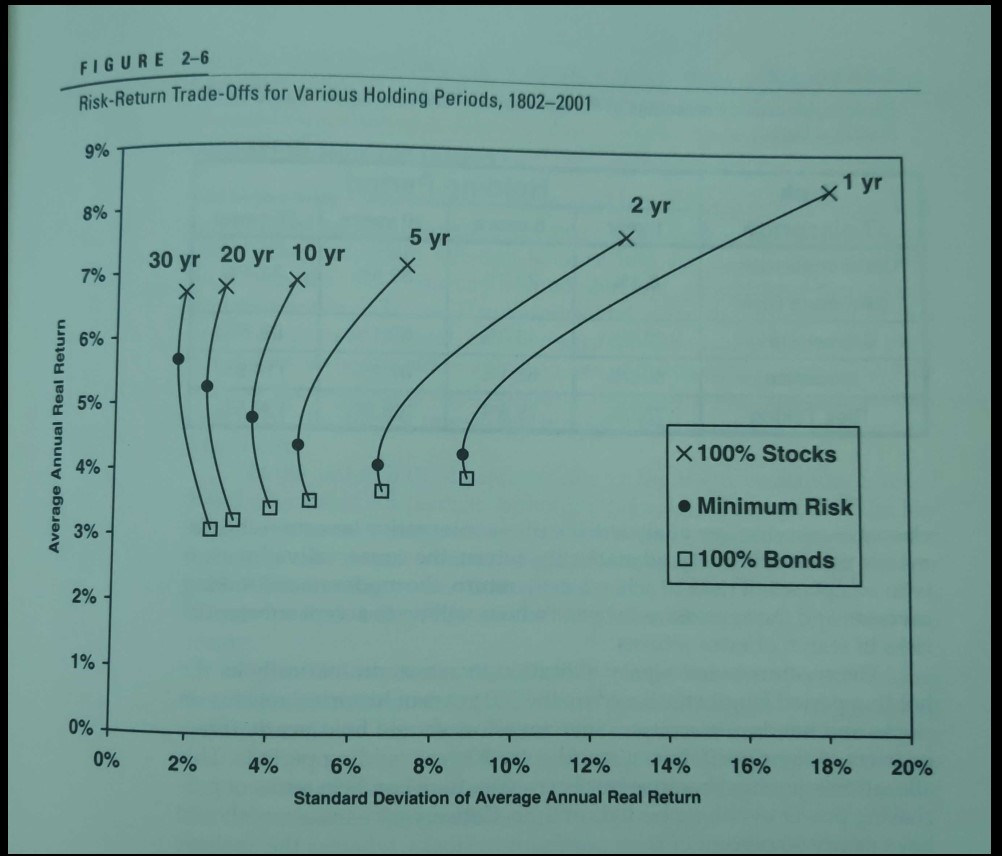

The chart below from the book Stocks for the Long Run showcases how both risk and return from 10 year onwards to 30 year is similar.

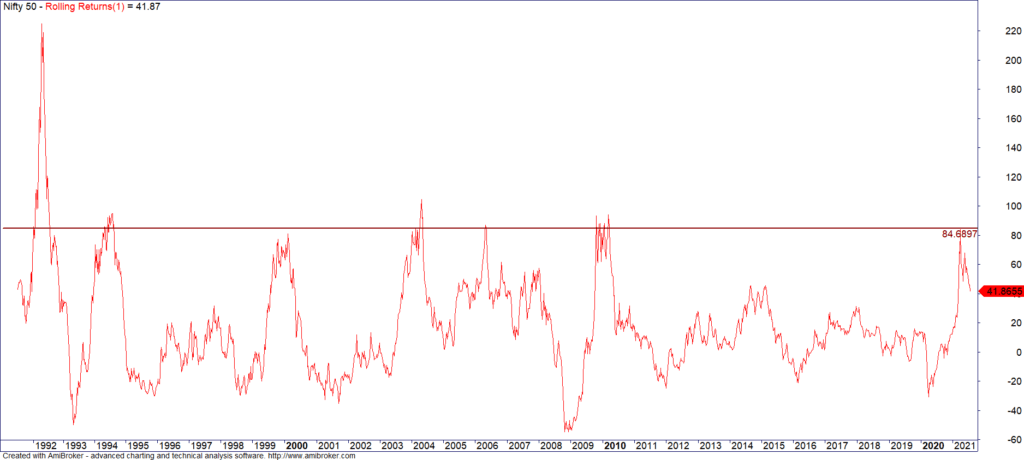

In April, the one year return for Nifty 50 was 84%. Let me show the rolling one year return to see the previous instances have had such insane returns in such a short period of time.

From 1992 onwards, we had multiple times when we had a one year return > 80%. The next one year returns on an average was negative 8.41%. But if I move the starting point to post 2000, the average return has been positive 11%.

When experts provide data, do note that it’s easy to mess around the same to meet the objectives or the viewpoints of the said expert. If I intend to promote why markets would remain bullish, just using data from 2001 onwards (20 years is long enough, right) suffices.

In the long run, Nifty 50 has given a return of around 12% and going into the future, we should not expect any difference.

If one were to invest today, the expectation has to be low. But one should invest in my opinion for there is no guarantee of an opportunity that can arise and one that can be taken advantage of. Waiting for a correction is good in theory but mostly bad when it comes to practice.

In March 2020, when Indices were down 40% from the peaks reached in January, the inflow into Mutual Funds was the same as in February when we had no worries with respect to Corona. In April, when the same opportunity was available with more clarity, Mutual Fund investments actually fell by half (vs the previous month).

Invest when there is blood in the streets, says Warren Buffett, but most of the time the blood is our own and even if we have the money to invest, we don’t have the courage. What this means is that we should invest when we are comfortable to invest rather than waiting for the best opportunity to come by.

If you don’t have the courage to invest a lump sum, split it into monthly SIP’s but do invest for even though Lump sum may be a better way vs SIP, both are better than staying put waiting for a crash to happen.

Recent Comments