In my last post on Nifty, I said that a swing trading system I use seemed to suggest a move to 6850 and that has been achieved. The question hence comes as to what next. On one hand, the mind being bullish, its tough to stay neutral and seek out whether there exists an opportunity for markets to fall. After all, I myself am a proponent of “Prediction is Impossible”, so it will be ironical if I start predicting where Nifty may go next.

Yesterday, Krishnakumar came out with his medium term target of 11000 on Nifty and while its easy to say that the target is too high, markets themselves have no memory of the past and forget 11000, even 16000 shall get achieved (its just a matter of time).

Coming back to Nifty, at 6850, are the markets over-heated. While on the short-term charts, many oscillators are indeed over-bought, on longer terms charts, there is still way to go before things become really overheated. For example, lets take RSI on the Monthly charts. As of now, its at 66 levels and 70 is considered to be the level above which markets are seen as over-bought.

But overbought doesn’t mean a sell. Those who have read John Haydens on this aspect would known that its actually a stronger buy above 60. And this is the first time RSI on the monthly charts has closed above 60 since 2010. During the runaway bull market during 2003 – 2007, RSI on monthly only once slid below the 60 mark (when Nifty fell due to NDA loosing the election and worse, Left having a hand in the power).

Markets follow a strong rally with a real long side-ways correction making the trader forget there had been one hell of a rally earlier and once could soon unleash once again. In fact, we become so used to this side-ways markets that when the real big one comes, we rarely are bullish since we cannot distinguish between this rally and the multiple previous ones that failed.

The 2003 – 2007 rally was not the first multi-year rally to occur in the Indian markets either. The biggest rally (if we are to take into account Sensex back-adjusted) happened between 1988 and 1992 when Sensex leapfrogged from sub 500 levels to 4500 level at the peak. Of course, after this we had a pretty long period without the high getting broken substantially. While the first break came in late 1999 / 2000, the bust of the .com in US meant that we had to wait for another 3 years before the older levels were broken once and for all.

After the peak in 2008, this is the first time we have closed above those peaks and hence its time to reflect as to whether this rally is similar to 2000 or 2003/07 for there in lies the question of whether Nifty will tough 11000 or 30000 (5x).

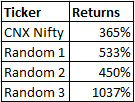

Unlike US, where there is ample amount of data on everything that has anything to do with markets, data is severely limited in India (unless you are prepared to shell out the big bucks and get yourself the best of the data feeds where you have access to a bit more data).

One way fundamentalists asses a stock is by looking at the Price Earnings Ratio. I have myself in my past Nifty posts used the same and here I post it updated till date

Markets have broken the previous high and currently is above its high of 2012 (Nifty high of 2012 was 6415 just for sake of comparison).

Markets top out on back of Euphoria and I see none. In fact, yesterday when the markets were rallying strongly, all brokers I know of had more sell orders than buy. While the same size is indeed small, the fact that retail are selling out of the rally just doesn’t fit into the theory of markets being in a bubble phase which shall get burst anytime soon.

Lets for a moment move out of Nifty chart and look at broader index charts. First comes the CNX Mid Cap

Forget about breaking 2008 / 2011 highs, this Index is just testing its 2013 highs as of now. Lets now head to the CNX Small Cap Index

Similar is the story out here as well. Its not yet testing the 2011 lows (which unlike Mid Cap Index is pretty far off from the 2008 highs).

And finally the CNX 500 Index

Story is a bit better but nowhere as good as CNX Nifty with its 2008 peak still being un-tested.

The reason for the wide difference (and this despite all these Indices being managed pretty efficiently by removing weak / dud stocks and inducting strong stocks) is due to the fact that this rally has been led by select sectors which were not the main drivers in 2008. Take Auto for instance. CNX Auto Index topped out in 2008 at near 2400 levels. Currently CNX Auto stands at 5950. CNX Pharma / CNX IT among too have a similar story to tell.

Once upon a time, Reliance was for the markets, what Tendulkar was for the Indian Cricket Team. Relaince moved the markets either way – a sort of bell weather. But today, no one cares about whether Reliance is up a percent or down since other stocks and sectors have firmly taken control of the Index.

For every fall and every rise, the public wants reason and the financial / media pundits are happy to oblige. Well before the 2008 bubble burst, small rises and falls were explained by Baltic Index, Japanese Yen among others. And right at that point of time, they seemed to be so correlated, that it made you wonder why you had not observed the same earlier. But while you were watching the statics that led the last rally / fall, markets and media had moved onto the next.

The US markets are on a free-fall as I write this (Dow down 200+ points). This even as today’s data point which was Jobless claims which came in lowest since 2007, theoretically a strongly bullish number, but wait, markets is focusing on something else for now and this hence takes a backseat. What the public evidently forgets is that Dow hasn’t seen a negative year since 2008. Even a 100 point fall would not do such a trend much harm.

According to the old adage, one should not lose sight of the forest for the trees. The markets is the forest that is made up of individual moves (trees). Its very easy to loose focus just at the moment you need to be totally focused. It comes down basically to the fact of what is your objective in the markets. Everyone is here for the money, but very few actually end up taking any part of it. Wealth Creation is the objective of most, but all I have seen is story after story of wealth destruction.

A friend of mine was repenting that the Mutual fund he sold off after holding for 3 long years (and getting back the sum invested) had seen its NAV move up by 10% right after he sold the damm thing. When expectations are high and instead we see a disappointment, its easy to miss the larger picture of this not being a time to sell but a time to maybe add to the investment.

A person who invests today with the 11000 target in mind will most likely end up in a loss, not because Nifty will not move to 11K, it will, but because, he is not prepared for the pain that may come in between the time. If markets were to drop from here by say 350 points (a 5% fall), more people will throw in the towel than what the number who expect to do that today.

A guy who buys Nifty today IMO has to be prepared to withstand (if he is a long term investor and not wanting to look at the daily moves), a pain threshold of at the very least 25% (average draw-down from year high). Even then, if 11K is indeed reached, its still a good risk reward set up (reward being 60% above current price).

And before I conclude, here is another chart which again seems to suggest that we aren’t in the topping out process as of now. This chart is a plot of the % of stocks trading above the 200 day EMA. To ensure that it doesn’t suffer from survivor-ship bias, I have used a database which has both running stocks and delisted stocks.

Between the first time it hit >70 numbers in 2009 till it finally made its high in 2011, Nifty appreciated by 40% and nope, it did not come without its fair share of drama :). And we had a negative divergence in his indicator to boot.

For quite some time I have held stead fast my belief that the time is not yet ripe for a rally of the kind we saw in 2003 or 2009 and have in an earlier post pointed out the same as well. One of my reasoning was that I felt that Modi was unlikely to become the next Prime Minister and markets will be dissapointed and be range-bound for the coming 2 – 3 years before we can see a massive rally.

But a look at the news as well as the odds supposedly offered for a Modi win seems to suggest that I am quite off the target in that prediction (though only the results can finally prove me right or wrong). The big question that needs an answer is, how shall the markets behave if Modi becomes a PM (since its more or less certain that markets will not take kindly to Modi not becoming a PM). Both in 2004 and 2009, markets surprised the expectations held by majority and this time shouldn’t be too different either. The only difference has been in the way markets have behaved in the months going into elections. While in the last two occasions, markets were more or less side-ways till the breakdown / breakout took place, this time, markets have already run up quite far and regardless of whether we fall from here or rise, we shall not see as much of a surprise as 2004 and 2009 was.

And now for bit of heresy 😉

Based on some statistical calculations, this is a note prepared for myself to see if Prediction is possible

Very High Probability (close to 100%) of Nifty falling 12% from its peak during 2014

50% Probability of Nifty falling 24% from its peak during 2014

11% Probability of Nifty falling 36% from its peak during 2014

Upper Range for Nifty – 7000 (High Probability), 9266 (Low Probability)

Assuming 7000 is reached and we form a peak round about there, we can then see a fall to 6160 (High Probability), 5320 (Medium Probability) or 4480 (Low Probability). Of course, all the above calculations are dependent on the peak we reach and changes as the peak value changes.

Adios for now, shall update my thoughts on Nifty after results are declared on the 16th of May.